McKinsey: rPET availability in the US market needs boost

According to a study by McKinsey, high long-term demand for recycled content in packaging could lead to shortages of recycled packaging materials in the US. Brand owners that are aiming to introduce new packaging formats and establish innovative ways to boost product recyclability and levels of recycled content to meet their sustainable-packaging commitments, address consumer concerns, and adapt to rapidly rising regulatory pressure could face the very real risk that they cannot achieve their goals because of an anticipated shortage of recycled materials: collection levels of high-quality recycled material look set to remain almost flat, creating supply challenges for brand owners and packaging companies, says the study.

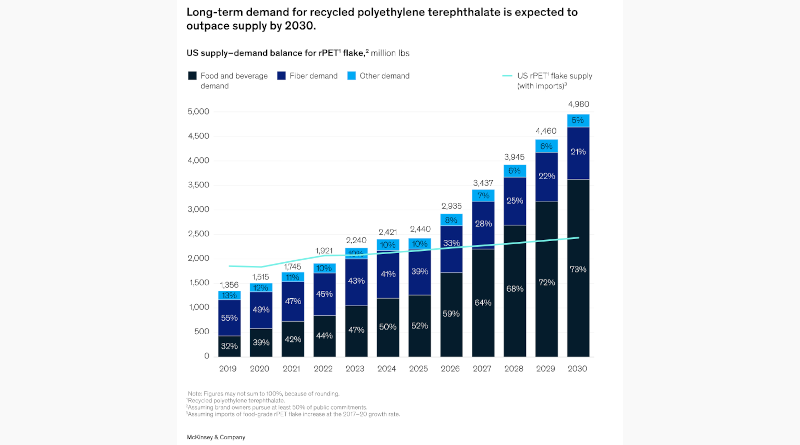

If brands with public recycled-content commitments follow through on their plans, the US demand for rPET in 2030 would outpace supply by about three times. As the supply-and-demand imbalance widens, the price premium between rPET and virgin PET has the potential to rise significantly over the next decade. The challenge for the industry moving forward will be to unlock additional rPET supply, the experts say and suggest three potential approaches, centered on boosting supply, ensuring access, and designing for circularity, that could also be applicable to other packaging substrates.

The experts have evaluated that today only about 27 per cent of PET bottles and about 18 per cent of all recyclable PET plastic waste is collected, the rest ends up in landfills. In recent years, the collection and sorting of PET has not improved significantly. As a result, rPET supply in North America grew only about 1 per cent per year in 2012-22. While there have been some new entrants in the recovery and reprocessing value chain, process losses have not been significantly reduced. This means that about 4.6 billion pounds of PET ends up in landfills every year.

Rapidly growing demand combined with stagnant supply could lead to a supply-demand imbalance for rPET in the future, the study outlines. Historically, rPET supply has only grown by about 1 per cent per year over 2012-22, while consumption has grown by about 4 per cent per year over the same period. If brands fully deliver on their recycled content commitments by 2030, demand for rPET is expected to grow by about 15 per cent per year between 2022 and 2030, the study says. Over the same period, supply is expected to continue to grow by only about 1 per cent, so that by 2030 demand will be three times higher than available supply.

In the future, ESG-driven use of rPET is expected to expand its market share and potentially lead to increasing price premiums as demand for rPET grows. In addition, brand owners may consider switching from other plastics – such as HDPE, PVC and PS – to rPET because it is more recyclable and considered more accessible compared to other plastics. This could lead to another supply shortage, the experts caution.

As future rPET availability will be determined by a combination of supply, demand and regulatory factors, packaging industry leaders should consider three meaningful ways to increase rPET availability, according to McKinsey:

Boost supply: With more than 80 percent of PET waste going unused, opportunities exist across the value chain to boost PET recovery, from collection through to sorting and processing. Given that recycling programs are often organized at the local level, there are opportunities to form public‒private partnerships to increase local collection rates in areas with underfunded or nonexistent curbside recycling. The Recycling Partnership, for example, is an organization that makes private investments in public recycling programs, with the aim of increasing the supply of recycled plastics. At the same time, investments in advanced sortation equipment at material recovery facilities are an additional avenue to increasing rPET supply. McKinsey also note that in some countries (such as the Nordic countries), national and state-level policies such as extended producer responsibility or deposit-return schemes are having a measurable influence on rPET supply.

Ensure access: As rPET becomes increasingly scarce, securing access to this substrate will become critical for brands hoping to meet their recycled-content commitments. The range of strategic options for companies will vary depending on the local policy and the location of their manufacturing plants and sources of rPET supply. For example, vertical integration with a recycler and long-term strategic partnerships or contracts with suppliers or competitors are viable models that we have seen work in the plastic-packaging industry and also for other substrates: for instance, several large paper manufacturers have their own integrated recycling operations. Moreover, there have also been several small-scale efforts by brands to directly recover their own bottles from consumers. Although currently uneconomic, this approach may become viable if the value of recycled materials continues to climb and access to supply becomes more difficult.

Design for circularity: Brands can accelerate their path to reaching circularity commitments by assessing what ways to improve packaging design to ensure material is recovered from the waste stream. Solutions here could range from moving away from colored PET to improving labeling and product design to encourage higher rates of consumer recycling. For instance, in July 2022, Coca-Cola announced that its Sprite brand would no longer use green-colored PET plastic, which has historically been harder to recycle into future food-grade bottle uses.

Authors: Maimouna Diakhaby, David Feber, Yasir Mirza, Daniel Nordigården, Brian Shields, Jeremy Wallach, all McKinsey