Second Icis Recycled Polymers Conference Asia

The 2nd Icis Recycled Polymers Conference Asia was held in Bangkok on February 21-22 and focused on the challenges, regulatory developments and collaborative opportunities in the field of plastics recycling in Asia, including rPET. The conference was attended by 74 CEOs, senior professionals and market influencers from across the supply chain from 14 countries.

General oversupply – weak demand for rPET

Icis analyst Joshua Tan Chee Yong and senior editor Arianne Perez opened the conference with an overview of installed capacity, price trends and outlook for 2023 and 2024 in Asia. In APAC, mechanical recycling is a large market with over 18 MTPY of installed capacity, while the more complex chemical recycling is just starting to emerge with only 700 KTPY of installed capacity (figures include rPET, rPE and rPP).

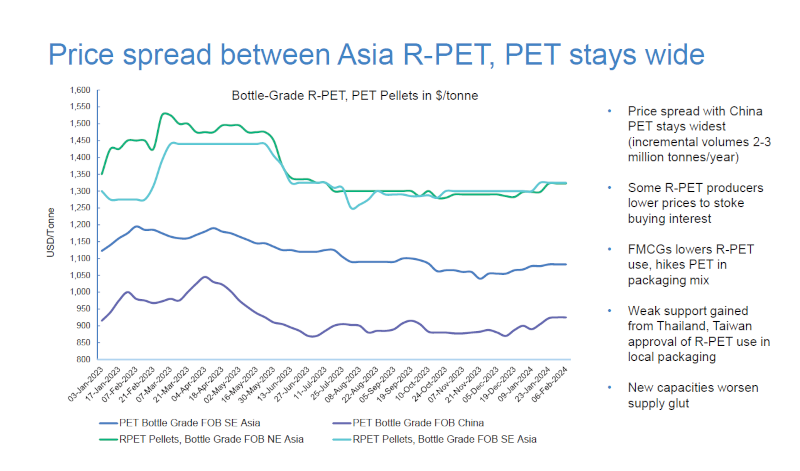

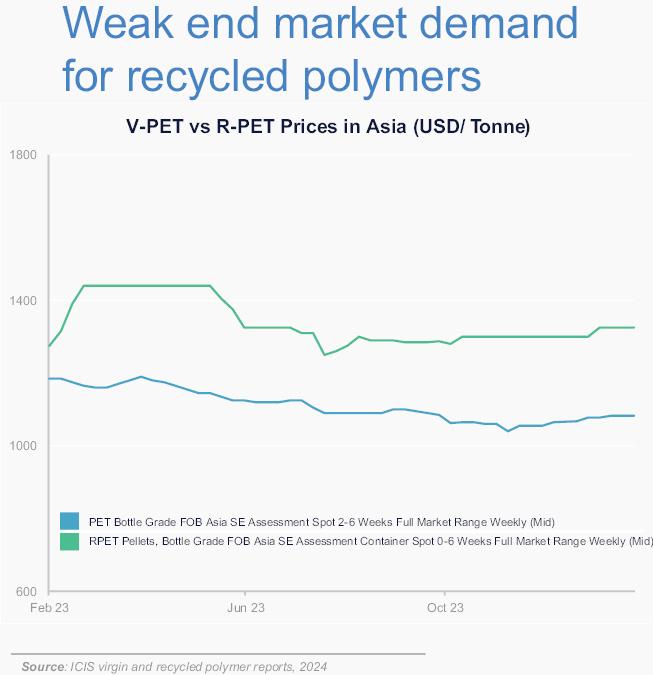

In 2023, the PET market experienced oversupply and weak demand for rPET. For most of 2023, there was a wide price spread between bottle-grade vPET from China and vPET in SEA (South East Asia), and an even wider spread between vPET from China and rPET in SEA and NEA. Increased PET production in China (an estimated 2-3 million tonnes of additional volume) contributed to this oversupply, flooding the market with cheaper PET and further reducing the attractiveness of rPET. In addition, rPET producers in SEA have also added new capacity, putting further pressure on prices. Weak demand from countries such as Thailand and Taiwan, where rPET is allowed in food packaging but not driven by sustainability targets or consumer pressure, has not helped.

While brands and established rPET producers can cope with reduced margins and are expected to survive the current situation, smaller and medium-sized rPET producers have already reduced production rates and cut prices to attract buyers. Bottle grade material is and will remain the most traded grade from Asia. Most produced rPET is destined for products for the European and US markets. Polyolefins, especially rPE/HDPE, face a similar situation of price pressure due to the large volumes of virgin material entering the market.

The outlook for 2024 remains weak: The general oversupply, the lack of sustainability targets or firm regulations in Asia on the mandatory use of rPET in packaging will continue to put pressure on the price of rPET.

Currently, Australia, New Zealand, Japan, South Korea, Thailand, India, Taiwan, Hong Kong and other major economies have approved the use of rPET in food packaging. In China, there are several food grade rPET players involved in mechanical recycling, such as Ceville, Yisheng Petrochemical, Guolong, Incom Recycle, Veolia and Alba. In addition, chemical recycling (via depolymerisation) is well established with companies such as Zhejiang Jiaren (DMT), SK Chemical & Shuye (BHET), Fujian Cyclone (BHET) and Yinjinda (BHET to PETG).

However, China remains one of the few countries that has not yet approved rPET for use in food packaging. Arnold Wang, Deputy Secretary General – China Packaging Federation, confirmed that many discussions and initiatives are underway and that people in the industry are eager to see progress. He expects something to happen this year.

Collection and sorting – the challenges with the informal sector

While countries such as Korea and Japan generally have some form of developed solid waste management system, countries in SEA and certain parts of the Indian subcontinent rely heavily on the informal sector and its waste pickers, bottle collectors, aggregators and possible middlemen. The particular challenges of sourcing raw materials from the informal sector were a key theme of the panel discussions and were also raised by several speakers.

Christian Pranata, CEO of the Langgeng Jaya Group in Indonesia, knows the Indonesian plastics recycling market well. His company, Langgeng Jaya, started recycling post-consumer PET in 2006. “Never stop buying” (even on major holidays), Christian Pranata said during a panel discussion, mentioning that he would rather accept warehouses fuller than needed than interrupt the recycling chain. It is clear that people in the informal sector, especially bottle collectors, depend on a regular and continuous, albeit small, stream of income. If this is not forthcoming, people will turn to any other kind of work to make a living.

Laurent Besson, General Manager of Veolia Services Indonesia, also recognises the challenge of collecting raw materials. In Asia, Veolia operates 14 plastics recycling plants with an annual capacity of 250,000 t for PET, HDPE, LDPE, PP and ABS. In Indonesia, the company recycles 1.2 billion bottles per year to produce 25 kt/y of food-grade rPET. The company’s PlastiLoop sustainability programme is designed not only to secure raw materials but also to support the informal sector by providing social and financial services (e.g. savings accounts), training, PPE equipment and uniforms to promote social recognition. To prove the origin and impact from raw materials to finished products, the company uses an end-to-end traceability system using blockchain technology.

Another sustainability programme in Indonesia is the Mahija Parahita Nusantara Foundation, a joint initiative between Coca-Cola Europe Pacific Partners Indonesia (CCEP Indonesia) and Dynapack Asia. It was the first closed-loop, food contact-approved PET bottle recycling facility in Indonesia.

In the Philippines, Coca-Cola and Indorama Ventures have launched the Tapon to Ipon initiative to supply clear PET plastic bottles to their joint venture, PETValue Philippines. The collection programme uses pop-up booths for post-consumer PET plastic bottles. Consumers can drop off (tapon) their used clear PET plastic bottles of any brand and receive incentives (ipon) in return.

The development of the rPET market in Thailand has only just begun. In 2022, the Thai Ministry of Public Health issued Notification No. 435, or “MOPH 435” for short, setting the standard to allow the use of PCR PET for food contact packaging. In 2023, three companies were approved and listed on the Thai FDA’s positive list. The first company was Envicco.

Envicco is a joint venture between PTT Global Chemical Public Company Limited, Thailand’s largest petrochemical company, and Alpla, the global rigid packaging specialist. The majority of the feedstock is sourced from the informal sector: drop points, local communities, schools, brand owners, waste community centres and micro-waste collectors.The project covers more than 45 provinces in Thailand. The installed capacity is 30,000 MTA of PCR PET (US FDA, EU EFSA and Thai FDA) and 15,000 MTA of PCR HDPE.

Natthanun Sirirak, Managing Director of Envicco, also shed light on the Thai FDA system, which has stricter safety criteria than the US FDA and the European Efsa in terms of raw materials and contamination levels. For example, the Thai FDA prescribes a maximum contamination level of only 210 ug/kg (US FDA 220 ug/kg) and no raw materials from landfills are allowed.

EcoBlue Ltd. Thailand, is another company that received rPET Thai FDA approval for food contact packaging applications. Made from 100% post-consumer waste, using state-of-the-art recycling equipment, including Starlinger’s Viscostar Solid State Polymerisation (SSP) system, and stringent quality controls, EcoBlue’s bottle grade rPET has also received US FDA and Efsa approval. The company also supplies specialty rPET for filaments, films, fibres and strapping, as well as food-grade recycled HDPE and PP.

No regulatory framework requiring the use of recycled content in packaging

In addition to reliance on the informal sector, there is another major difference to the European and US recycling markets. There are no regulatory frameworks requiring the use of recycled content in packaging. Therefore, rPET has to be a cost effective alternative to virgin material, which it is not. As a result, the recycling sector is heavily reliant on major global brands committing to increase the amount of rPET in their bottles, either to meet the EU’s 25% target by 2025, as an internal corporate commitment or as a marketing strategy. However, the regulatory framework and consumer pressure are lacking.

Bridging the circularity gap – PET through chemical recycling

With a general lack of regulatory frameworks and higher operating costs compared to virgin material production, the capital-intensive chemical recycling process faces significant hurdles in SEA and NEA. But there are success stories.

Japan’s Jeplan, founded in 2007, has been at the forefront of plastics recycling, with previous efforts in PET clothes-to-clothes recycling and commercial plant operations. In 2020, the company entered into a strategic partnership with technology provider and licensor Axens to develop an innovative recycling process called Rewind PET. In October 2023, Jeplan commissioned a 1,000 t/a (1 kta) PCR PET chemical recycling plant in Japan. The process can be used to recycle all types of PET waste, especially those that are difficult to recycle mechanically, such as dark and black PET materials, coloured and opaque bottles, multi-layer trays, packaging film and polyester textiles. Through continuous depolymerisation and deep cleaning, the process produces high quality BHET (bis(2-hydroxyethyl) terephthalate) monomer, ensuring a virgin-like quality suitable for a wide range of PET applications, including food applications.

The company’s chemical recycling efforts are also beginning to bear fruit. One of the first batches of rPET was immediately sold to a high-profile customer. Outdoor clothing specialist Patagonia is using its rPET to work towards eliminating all virgin polyester from its products by 2025.

Others

Participants and speakers were rather united when it came to DFR (Design for Recycling): No coloured bottles (clear or clear and light blue in a 70/30 ratio), mono-PET material, labels must be easy for the consumer to remove, no full-sleeve labels, no self-adhesive labels and no direct printing because of the risk of heavy metals in the colour pigment. PVC, but also PET-G, were mainly considered as problematic materials.

The conference also covered topics such as legacy MSW (Municipal Solid Waste) Bio-mining (an environmentally friendly technique for separating soil and recyclable materials such as plastic, metal, paper and textiles) with an EPR perspective.