New IMARC report: Australia’s PET bottle market to reach US$487.8M by 2033

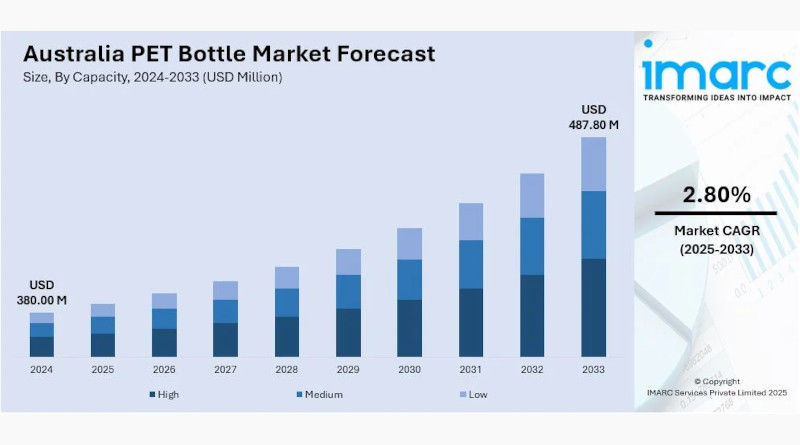

The Australian PET bottle market, valued at USD 380 million in 2024, is projected to reach USD 487.8 million by 2033, growing at a CAGR of 2.8% from 2025–2033, according to the new market research report Australia PET Bottle Market Size, Share, Trends and Forecast by Capacity, Color, Technology, Distribution Channel, End Use, and Region, 2025-2033 from IMARC Group.

The Australia PET bottle market share is witnessing significant growth as consumers are demanding lightweight, durable, and recyclable packaging solutions across the food and beverages (F&B), personal care, pharmaceuticals, and consumer goods industries. A significant driver for market expansion is the rising preference for bottled water and functional beverages, fueled by heightening health awareness and changing lifestyles. As the F&B industry represents a major consumer of PET bottles, demand keeps on increasing in line with boosting production as it has become inexpensive and clear packaging material that effectively retains the product’s integrity. Further growth has been accelerated with the expansion of the e-commerce sector, in which PET bottles exhibit superior breakage resistance while providing lower shipping costs than its competitor, glass. In addition, manufacturers are being prompted to include rPET in their packaging due to the intensifying regulatory emphasis on sustainability and extended producer responsibility, all which Australia is encouraging through its ambitious national packaging targets toward 100% recyclable, reusable, or compostable packaging.

Technological advancements in manufacturing PET bottles, such as the development of lightweight and high-barrier bottles with enhanced recyclability, support Australia PET bottle market growth. Additionally, bio-based PET production innovations, along with the integration of circular economy principles, have further spurred industry expansion because the companies are trying to reduce dependence on virgin plastic and lower carbon footprints. Moreover, commitment from the Australian government to policy measures such as the National Plastics Plan and container deposit schemes encourages investments in PET recycling infrastructure, fostering a closed-loop system that enhances raw material availability. Multinational beverage companies, along with local players, have increasingly shown a trend toward sustainable packaging, boosting demand for PET bottles made of post-consumer recycled (PCR) content. The expansion of the dairy and plant-based beverage market and the accelerating consumption of ready-to-drink products have even promoted the PET bottle adoption since the hot-fill and aseptic processing technologies allow for stability and amplified shelf life for the product.

Australia PET bottle market trends:

Rising demand for sustainable and recyclable packaging

There is a new trend in Australia PET bottle market outlook, driven by government regulation and consumer preference demands, along with corporate initiatives for sustainability. The Australian Packaging Covenant Organisation (APCO) has committed to making all packaging 100% recyclable, reusable, or compostable by 2025, prompting beverage and FMCG companies to enhance their way toward rPET bottles. The country’s CDS further encourage PET recycling, increasing collection rates and demand for high-quality recycled content. Advances in PET bottle manufacturing, including lightweighting and bio-based PET, also contribute to lower material consumption and enhanced recyclability.

Growth of the bottled water segment

A strong rise in a health-conscious customer base is promoting the growing trend of Australians, which focuses their attention more on convenient methods for hydration that promote the sales of bottled water directly affecting demand of PET bottles. Market development through awareness toward hydrated living fitness issues and awareness for the issue that some states water quality becomes unsatisfactory or unpotable. Premium and functional water categories, such as alkaline, electrolyte-enhanced, and vitamin-infused water, are also becoming popular, accelerating the consumption of PET bottles. The tourism and hospitality industry is also one of the main contributors to the increasing demand for bottled water, as visitors and travelers look for convenient hydration solutions that are easy to carry.

Technological advancements in PET bottle manufacturing

The Australia PET bottle market forecast has experienced a new wave of technology with the introduction of innovations towards increased efficiency of production, sustainability, and greater flexibility in bottle designs. Better strength in bottles, along with decreased plastic consumption, is obtained with advanced blow moulding techniques: injection stretch blow moulding (ISBM) and extrusion blow moulding (EBM). Improved efficiency in high-speed filling lines and energy-saving equipment in the manufacturing process minimise operating costs of beverage and FMCG companies. These enable customisation, brand differentiation, and personalised packaging solutions, thus adapting to evolving consumer preferences. On the other hand, innovations in barrier technologies – oxygen scavengers and multilayer PET structures – allow longer shelf lives of beverages and give PET bottles more competitive advantage than alternative materials. With amplified investments in smart packaging solutions, such as QR-coded bottles for traceability and interactive engagement, PET packaging manufacturers are aligning their offerings with modern consumer demands while maintaining regulatory compliance and sustainability commitments.

Australia PET bottle industry segmentation

IMARC Group provides an analysis of the key trends in each segment of the Australia PET bottle market, along with forecasts at the country and regional levels from 2025-2033. The market has been categorised based on capacity, colour, technology, distribution channel, and end use.

Capacity: High-capacity PET bottles over 1L are becoming popular in the areas of bulk water, carbonated beverages, and household products. The reason behind the increased popularity is for cost efficiency, reduced packaging waste, and convenience of using it for a longer time. Manufacturers are striving for making the packages lighter and incorporating rPET into the bottles to ensure durability and performance. Bottled water, soft drinks, and functional beverages markets are dominated by medium-capacity PET bottles with a volume of 500ml to 1L. Such a balance between portability and volume makes it suitable for on-the-go consumers. Brands highly use ergonomic designs, smart packaging, and increased post-consumer recycled content to meet both sustainability goals and evolving consumer preferences. Low-capacity PET bottles, below 500ml, are found to be used for impulsive purchases, on-the-go beverages, personal care products, and the like. Broad application in energy drinks, flavoured water, and cosmetics is expected to maintain steady demand.

Colour: PET bottles are very transparent and widely used in the beverage industry, especially in bottled water, soft drinks, and juices, since they improve the visibility of the product and trust from the consumer. Their high recyclability makes them popular for sustainability-focused initiatives, such as mounted rPET usage. Brands invest in UV protection coatings and lightweight designs to maintain product integrity and environmental compliance. Coloured PET bottles are utilised intensely for dairy, personal care, and pharmaceutical products providing protection against UV and visual brand differentiation.

Technology: Stretch blow moulding dominates PET bottle manufacturing in the beverage industry. For non-beverage sectors like personal care and pharmaceuticals, extrusion blow moulding allows complex shapes and multi-layer designs, though with recyclability challenges. Thermoforming is mainly applied to PET trays and containers, offering cost-effective and lightweight packaging, with research underway on biodegradable and recyclable options. Emerging technologies, including 3D printing and hybrid moulding, support customisation, small-batch production, and innovative designs, aligning with circular economy goals.

Distribution channel: B2B dominates Australia’s PET bottle market, supplying major beverage, personal care, and pharmaceutical companies with large-scale, customised, and eco-friendly packaging, driving demand for rPET and lightweight bottles. Retail channels — supermarkets, convenience stores, and e-commerce — fuel consumer demand, particularly for bottled water and functional drinks, with online sales boosting single-serve and sustainable packaging trends.

End use: Packaged water is the largest segment, driven by health-conscious consumers, rising incomes, and water quality concerns, with brands adopting rPET and lightweight designs. Carbonated soft drinks remain key, supported by durable, CO₂-retaining bottles and sustainable formats. Food bottles and jars benefit from PET’s transparency and safety, with investments in tamper-evidence and longer shelf life. Non-food uses span personal care, household, and pharma, increasingly shifting to bio-based and recyclable PET. Fruit juice packaging leverages barrier technologies and aseptic filling for freshness, while beer in PET grows for outdoor and travel use despite recyclability challenges. Other applications include dairy, energy drinks, and homecare, supported by demand for functional beverages and sustainable, smart packaging.

The report also examines the regional landscape across ACT & NSW, Victoria & Tasmania, Queensland, Northern Territory & South Australia, and Western Australia, alongside detailed insights into the competitive environment, latest industry developments, and future growth opportunities.