PET recycling infrastructure in Europe – current capacity

The PET recycling process starts with the arrival of the material (i.e. PET bales) to the recycling facility, where it is shredded and washed, producing flakes. Flakes can be either directly commercialised by recyclers (for applications such as packaging) or be sent to extrusion into pellets.

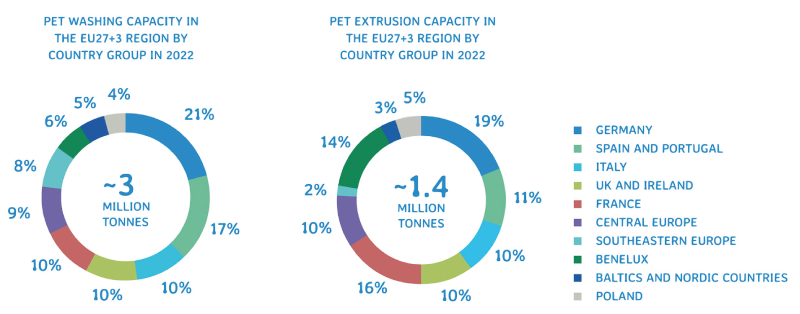

The first point of the PET recycling value chain where it is possible to measure how much PET can be recycled is the material washing step. The installed washing capacity in the EU27+3 region was around 3 million tonnes in 2022, which accounted for almost 25% of the installed plastics recycling capacity for all polymers. This was an addition of 200,000 t to PET washing capacity in relation to 2020. The first figure below shows the installed washing capacity per country group, with Germany accounting with the largest share of about 630,000 t, followed by Spain & Portugal with almost 500,000 t capacity. Italy (307,000 t), UK & Ireland (292,000 t) and France (286,000 t) are the next countries with the largest capacities. Together, these seven countries account for approximately 67% of rPET flake production capacity. Spain, Germany and Romania witnessed the highest capacity growth between 2020 and 2022.

PET polymer recycling capacity for flakes production (washing capacity) has the highest average recycling capacity per plant across all polymers, averaging over 20,000 t per facility, with Benelux, Germany and France having a higher average plant size in terms of geographies. The second figure shows that the extrusion capacity for rPET pellet production from flakes was estimated at around 1.4 million tonnes in 2022, representing a two-fold increase since 2020. This capacity, which absorbs the majority of flakes from the market to extrude into material suitable for food contact applications (mainly food grade pellets), has developed with the demand for rPET materials to comply with mandated targets and voluntary commitments from brand owners and has driven significant investment in this sector of the value chain. Germany accounts for the largest share at over 270,000 t, followed by France (220,000 t) and Benelux (200,000 t). Of the 140 companies reprocessing PET waste into flakes in EU27+3 in 2022, about 40 are integrated with downstream extrusion capacity to produce rPET pellets, i.e. the plant has both washing and extrusion processes.

Additionally, over 20 companies only produce pellets from flakes procured from external sources. Thus, about 60% of the rPET extrusion capacity in the region is integrated upstream with flake production, having both washing and extrusion lines within the same facilities. As seen in figures below, the geographical areas of Benelux and France have the highest installed extrusion capacity in relation to the washing capacity, indicating sufficient domestic capacity to convert flakes into pellets locally. Domestic recycling capacity has developed strongly since 2020, with overall available volumes matching demand as set by mandatory recycled content targets for 2025. However, due to the disparity in collection systems across the member states, some capacity was not able to reach its potential due to a lack of available quality feedstocks. Any subsequent gap in supply was met by imports during 2022, with significant increases in rPET flake and pellet imports throughout the year. This displaced domestic supply as the market balance shifted out of typical seasonal patterns, whereby demand spiked early in the year when due to the low season for beverage consumption bale availability was equally low.